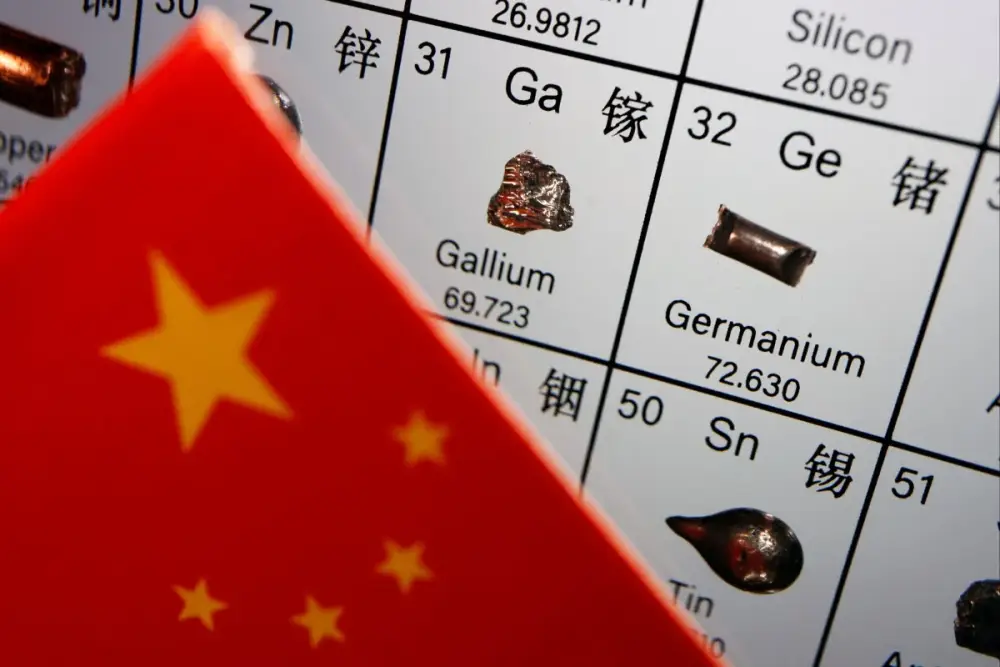

Sự thống trị của đất hiếm của Trung Quốc phải đối mặt với sự phản đối toàn cầu nhưng Bắc Kinh có 'bàn tay mạnh mẽ'

-

Trung Quốc gần đây siết chặt xuất khẩu đất hiếm, khiến các nước đẩy mạnh đầu tư để đa dạng hóa nguồn cung và giảm phụ thuộc vào Bắc Kinh.

-

Dù vậy, Trung Quốc vẫn xử lý tới 90% đất hiếm toàn cầu và chiếm 69% sản lượng, tạo ra lợi thế đáng kể về định giá và kiểm soát thị trường.

-

Vào ngày 2/7, công ty St George Mining (Úc) công bố bắt đầu xác định khu vực giàu khoáng tại dự án Araxá ở Brazil, tập trung vào đất hiếm và niobi.

-

Trước đó, hai công ty Mỹ là Kaz Resources và Cove Kaz Capital công bố hợp tác với công ty địa chất quốc gia Kazakhstan để khai thác dự án Akbulak.

-

Critical Metals Corp (niêm yết tại Nasdaq) nhận khoản vay đến 120 triệu USD từ Ngân hàng Xuất - Nhập khẩu Mỹ để đầu tư dự án đất hiếm ở Greenland.

-

Lynas Rare Earth (Úc) hiện là nhà sản xuất duy nhất ngoài Trung Quốc cung cấp oxide dysprosium tách riêng, hoạt động tại Malaysia.

-

Chính phủ Ấn Độ công bố kế hoạch đầu tư 35-50 tỷ rupee (408-583 triệu USD) để tăng sản lượng đất hiếm trong tháng 7.

-

Mỹ ký thỏa thuận với Ukraine vào tháng 5 để thúc đẩy đầu tư dài hạn vào khai thác khoáng sản.

-

Theo Earth Rarest, Úc có thể cung cấp 15-20% nguyên tố neodymium và praseodymium toàn cầu (trừ Trung Quốc), nhưng không thể thay thế hoàn toàn 17 nguyên tố đất hiếm.

-

Việc giảm phụ thuộc Trung Quốc gặp thách thức lớn về chi phí (ít nhất hàng nghìn tỷ USD), thời gian (10-20 năm) và thiếu hụt nhân lực chuyên môn.

-

Trung Quốc vẫn có "quyền lực mạnh" nhờ chiến lược nhà nước và khả năng tạo bất ổn tài chính để trì hoãn các dự án cạnh tranh.

📌 Trung Quốc vẫn giữ thế thống trị trong chuỗi cung ứng đất hiếm, xử lý 90% sản lượng toàn cầu và kiểm soát giá. Dù nhiều quốc gia từ Mỹ, Úc, Kazakhstan đến Greenland đang đầu tư lớn, các chuyên gia cảnh báo quá trình thay thế cần ít nhất 10-20 năm và chi phí khổng lồ. Khả năng phản công thực tế vẫn còn hạn chế nếu thiếu chiến lược tài chính và nhân lực toàn cầu.

https://www.scmp.com/economy/china-economy/article/3317330/chinas-rare-earth-dominance-faces-global-pushback-beijing-has-strong-hand-analysts

China’s rare earth dominance faces global pushback but Beijing has ‘strong hand’: analysts

From Ukraine to Kazakhstan, new investments target Beijing’s grip on critical minerals – but analysts warn it could still lead for years

How critical minerals became China’s ultimate trump card in the trade war

Beijing’s recent export controls on rare earths have spurred a flurry of international efforts to diversify supply chains and reduce China’s long-standing dominance in critical minerals.

On July 2, the Australia-listed St George Mining announced in an email that it had begun identifying enriched mineral zones at its fully-owned Araxá niobium-rare earth elements project in Brazil.

Two weeks earlier, US companies Kaz Resources and Cove Kaz Capital issued a statement about their partnership with Kazakhstan’s national geological company to explore and hold metallurgical tests at the Akbulak rare earth project.

Governments have also moved to boost production or secure critical mineral supply chains.

Earlier in July, the Times of India reported that Delhi would invest between 35 billion (US$408 million) to 50 billion rupees to increase rare earth output.

In Australia, research firm Earth Rarest said the country could become the world’s second-largest source of light rare earths, potentially supplying 15 to 20 per cent of neodymium and praseodymium – excluding China.

But it cautioned that the country could not “fully replace” China across all 17 elements.

ll continue holding the cards for quite a while,” said Vivek Y. Kelkar, an independent analyst based in India. “The attempt to minimise China’s dominance in REEs began a few years ago, but it hasn’t moved far enough to talk about the end of Chinese domination in the sector.”

“The sheer amount of time needed is at least 10 to 20 years, [and] it costs at least trillions,” he said.

“Where are the talents going to come from? Who understands how to process these materials? Who understands how the refining process works? How to get the purities? Those talents don’t exist in most places.”

Few countries have proposed effective state-backed or state-driven investment strategies, Kelkar said, which would give China “a very strong hand” for the foreseeable future – unless global finance can be “effectively channelled”.

“The next stage of [the] US-China rivalry will intensify across global REE mining and sourcing, specifically focused on regions in Africa and Latin America,” he added, pointing to growing US initiatives in Angola, Rwanda and Saudi Arabia aimed at securing supply chains.

Thảo luận

Follow Us

Tin phổ biến